SK Hynix Overtakes Samsung: The Chip War Just Got Real

"SK Hynix surged 5.6% to become South Korea's most valuable company, dethroning Samsung. AI demand for memory chips is reshaping the semiconductor pecking order. What this means for your portfolio and the chip sector."

The Chip War Just Got Interesting

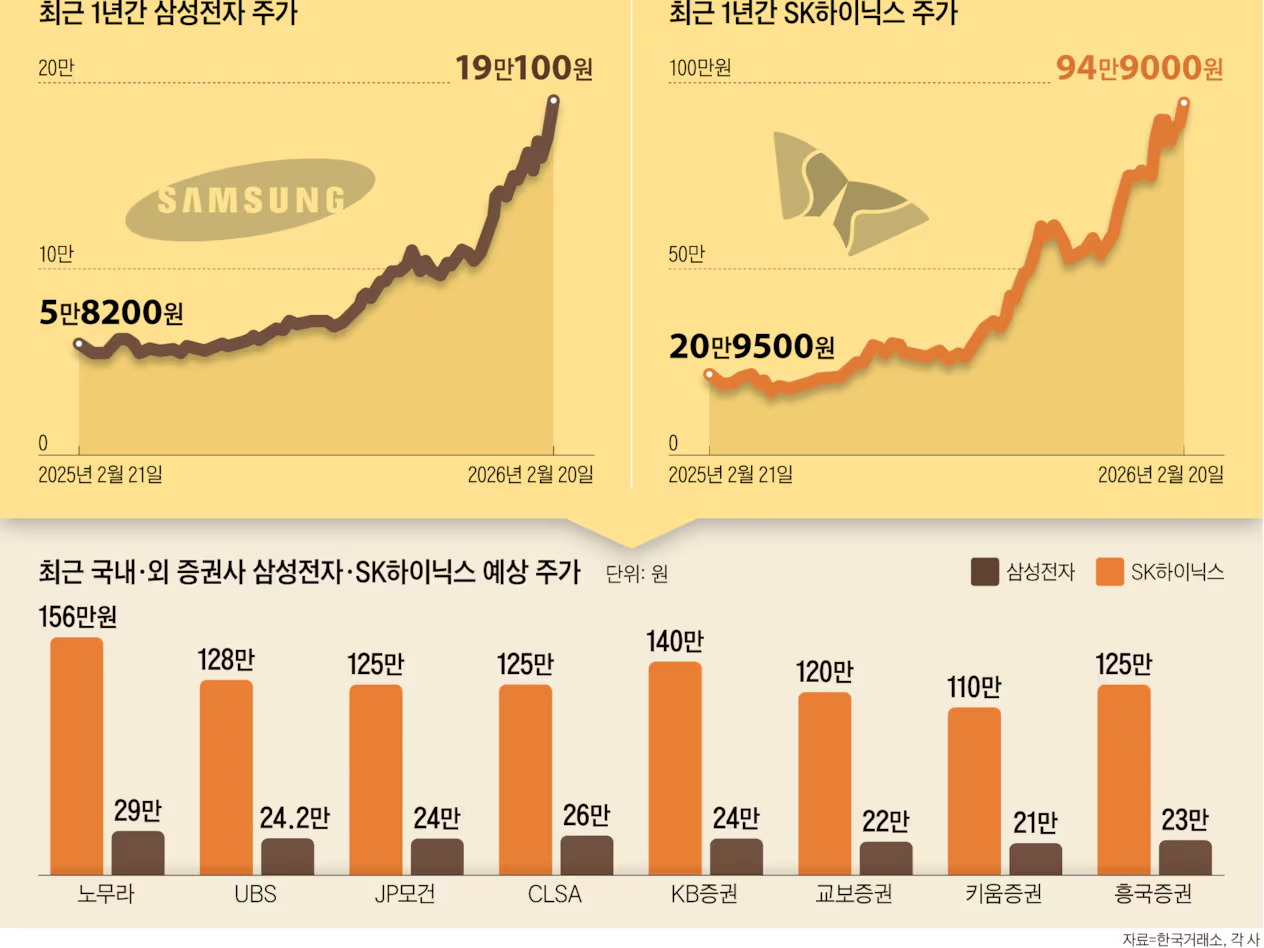

Here's something that doesn't happen often. A company just dethroned Samsung as South Korea's most valuable corporation. And not by a little. SK Hynix is now the king.

SK Hynix popped 5.6% today. That's a massive move for a mega-cap stock. And it happened for one reason: the memory chip shortage is back, and SK Hynix is positioned to make a killing.

Most traders are still sleeping on this story. They're obsessed with Nvidia and the fancy AI chips. But here's the thing—you can't run an AI data center without memory. And SK Hynix makes the best DRAM and NAND flash in the world.

Why This Matters More Than You Think

Samsung's been the king for decades. It's THE Korean tech giant. But Samsung got caught flat-footed on AI demand. They didn't ramp production fast enough. Meanwhile, SK Hynix? They saw the wave coming and positioned accordingly.

Now enterprises building AI data centers need memory desperately. And SK Hynix is one of the only suppliers who can deliver. That's leverage. That's pricing power. That's profit margins expanding.

When one company dethrones another that's been dominant for 30 years, it signals something structural shifted. This isn't a temporary move. This is market share changing hands.

The Semiconductor Pecking Order is Shifting

For years it was: Nvidia (GPUs) → Samsung (memory) → Intel (CPUs) → everyone else.

Now it's: Nvidia (GPUs) → SK Hynix (memory) → Samsung (struggling) → Intel (rebuilding).

This matters because SK Hynix is way more undervalued than Nvidia. While everyone was chasing Nvidia at $200+, SK Hynix was quietly executing. Now they're reaping the rewards.

What Traders Should Watch

1. Memory Chip Pricing

If SK Hynix can maintain high prices while ramping volume, profit margins go parabolic. That's the bull case. Watch their quarterly guidance.

2. Samsung's Response

Samsung won't take this lying down. They'll invest billions to catch up. But that takes 6-12 months. SK Hynix has the window right now.

3. Other Memory Players

Micron (MU) and Kingston are the other players. If SK Hynix is winning, Micron gets some demand too. Both could rally.

4. Geopolitics

Here's the risk. Both SK Hynix and Samsung are South Korean companies. If China-Taiwan tensions escalate, both get hit. But SK Hynix has more exposure to China.

The Real Play

Don't chase SK Hynix here. It just jumped 5.6%. But on any pullback, this is a solid position.

The memory chip sector is cyclical. It's in the early stages of the cycle right now. Prices are high, demand is strong, supply is tight. This lasts 18-24 months typically.

Micron (MU) is the other way to play this. It's a US-listed company with less geopolitical risk. Both SK Hynix and Micron could see significant upside over the next year.

The AI boom isn't just about Nvidia. It's about the whole supply chain. Memory chips are often forgotten, but they're the backbone of every data center.

Right now, SK Hynix is the beneficiary. And Samsung's struggling. That's a rare shift. Trade it accordingly.

💰 Memory Chip Shortage = Pricing Power & Margins

SK Hynix controlling supply of DRAM & NAND flash. High prices + strong demand = profit expansion for next 12-18 months

For 30 years Samsung was the king. Today, SK Hynix takes the crown. What's next for the chip sector? 💾

FAQ - SK HYNIX & MEMORY CHIPS

Q1: Why did SK Hynix jump 5.6%?

Became South Korea's most valuable company, dethroning Samsung. Market recognizes memory chip demand is explosive and SK Hynix is best positioned.

Q2: What does SK Hynix make?

DRAM (memory for computers) and NAND Flash (storage). Essential for AI data centers, servers, smartphones, everything.

Q3: Why is Samsung losing to SK Hynix?

Samsung was too slow ramping AI-focused memory. SK Hynix saw the trend coming and executed faster. Simple as that.

Q4: Can Samsung come back?

Yes, but it takes 6-12 months to ramp production. SK Hynix has the window right now. Samsung will catch up eventually.

Q5: Is this a permanent change or temporary?

Likely permanent. Chip cycles last 18-24 months. SK Hynix will dominate memory for the next 1.5-2 years minimum.

Q6: Should I buy SK Hynix stock?

Already up 5.6% today. Wait for pullback. But yes, it's a solid long-term play. Memory demand is structural, not cyclical.

Q7: What about Micron (MU)?

Micron is the US alternative. Less geopolitical risk than SK Hynix. Could also benefit from memory shortage. Good hedge.

Q8: Is memory shortage good or bad for my portfolio?

Good if you own SK Hynix or Micron. Bad if you own companies that need cheap memory (AI startups, servers, etc.).

Q9: Why didn't anyone see this coming?

Everyone was obsessed with Nvidia GPUs. Memory chips are boring. But boring + essential = profitable.

Q10: How much higher can SK Hynix go?

If memory pricing stays high: 20-30% upside from here. If pricing normalizes: flat to down 15%.

Q11: What's a fair valuation for SK Hynix?

P/E of 8-10x is reasonable for a cyclical chip company. That gives 15-20% upside over 12 months.

Q12: Should I short Samsung?

No. Samsung is diversified (displays, consumer electronics, batteries). It won't collapse. But growth will be slower than SK Hynix.

Q13: What about NAND flash specifically?

NAND flash is tight supply. AI servers need massive storage. Pricing is strong. This is the profit driver for SK Hynix.

Q14: Is China a risk for SK Hynix?

Yes. SK Hynix has exposure to China. If US-China tensions escalate, SK Hynix could get hit. Micron is safer geopolitically.

Q15: How does this affect Nvidia?

Positive. More memory supply = more data centers get built = more GPUs sold. Rising tide lifts all boats.

Q16: Should I buy memory chip stocks instead of Nvidia?

Different risk profiles. Nvidia is growth play. SK Hynix is value play with cyclical upsides. Own both.

Q17: When does the memory shortage end?

18-24 months from now (late 2027 / early 2028). Then pricing normalizes and margins compress.

Q18: What happens to memory prices when shortage ends?

They collapse 30-50%. That's why timing matters. Sell SK Hynix before the shortage ends.

Q19: Is SK Hynix profitable right now?

Yes. Strong cash flow, positive earnings. Not like Nvidia which has high multiples. SK Hynix is cheaper on fundamentals.

Q20: Should I buy on the 5.6% pop?

No. Buy on pullback to $40-45 if you want entry. Right now it's momentum trading.

Q21: What's the dividend yield on SK Hynix?

Around 2-3%. Not huge, but steady income while you wait for price appreciation.

Q22: Is this a long-term hold or short-term trade?

Long-term hold (12-18 months). Memory cycle is long. But take profits before cycle peaks.

Q23: What if AI demand slows?

Memory demand slows too. Prices fall. Margins compress. SK Hynix stock drops 20-30%.

Q24: How does PCE data Thursday affect memory chips?

If PCE is hot = rate hikes = AI company capex slows = memory demand weakens. Inverse relationship.

Q25: Should I hedge SK Hynix with puts?

If you own it, yes. Put options are cheap insurance. Protects downside if memory cycle ends early.

Q26: What about Japanese chip makers (Sony, Kioxia)?

Smaller players. SK Hynix and Micron are the duopoly. Japanese makers can't compete on scale.

Q27: Is this geopolitical risk worth it?

For aggressive traders, yes. 20-30% upside over 18 months beats many alternatives. For conservative investors, stick with Micron.

Q28: What's the biggest risk?

China escalation. If US restricts chip sales to China, SK Hynix gets crushed. Geopolitical risk is real.

Q29: Should I tell my friends to buy SK Hynix?

Only if they understand chip cycles. Memory stocks are cyclical. Timing is everything. Most retail investors get this wrong.

Q30: What's your prediction for SK Hynix in 6 months?

Up 15-25% if memory cycle continues. Down 10-15% if PCE is hot and rate hikes accelerate. My bet: up 20%.